Market Report

Winter Market Report: Property Insights

5 June 2026

by Sally O'Connell, Chief Executive Officer

A more selective market, regional resilience and opportunity for well-advised buyers

Australia enters Winter 2026 with the housing market still showing resilience, but with a more measured tone than at the start of the year. National home values were flat in May, following a progressive loss of momentum across most markets. Beneath the headline result, conditions remain distinctly varied. Sydney and Melbourne are leading the softer conditions, while Perth, Darwin, Brisbane, Regional Western Australia and parts of Queensland continue to record stronger gains.

This is no longer a simple story of undersupply pushing prices higher across the board. Supply remains important, and new housing delivery continues to be constrained by elevated construction costs and feasibility challenges. However, demand-side pressures are now more visible. Affordability remains stretched, interest rates have moved higher, inflation has proven persistent, consumer confidence remains weak, and policy uncertainty around property investment has weighed on sentiment.

The macro backdrop has also become more challenging. The RBA lifted the cash rate by 25 basis points to 4.35% in May, citing inflationary pressure, tight labour market conditions and heightened global uncertainty. Inflation remains above the RBA’s target band, while the labour market is beginning to soften. Consumer sentiment has improved slightly from recent lows, but households remain cautious.

Although the latest housing data largely predates the Federal Budget, the proposed property investment changes have had an immediate impact on sentiment. Investor activity has softened, first-home buyers are seeing less competition in some auction environments, and both buyers and vendors are taking time to reassess the outlook. As a result, transaction volumes have eased as the market works through the immediate and medium-term implications.

For housing, the result is a more selective market rather than a weak one. The best homes in the best locations continue to attract committed buyers, particularly where presentation, pricing and campaign strategy are aligned. However, buyers are now more disciplined, more finance-sensitive and more prepared to wait where price expectations feel stretched.

For vendors, this means the market still has depth, but not unlimited depth. Strong outcomes will increasingly depend on clear price guidance, careful preparation and campaign discipline. For buyers, improving conditions are creating more choice and, in some cases, a better opportunity to secure quality property without the same level of urgency seen in stronger growth cycles.

In this environment, experience matters. A more selective market rewards trusted advice, local knowledge, strong negotiation and the ability to read buyer behaviour clearly. For Abercromby’s clients, it is a market that still offers opportunity, but it is a market where strategy will make all the difference.

Capital city performance: the market has split sharply

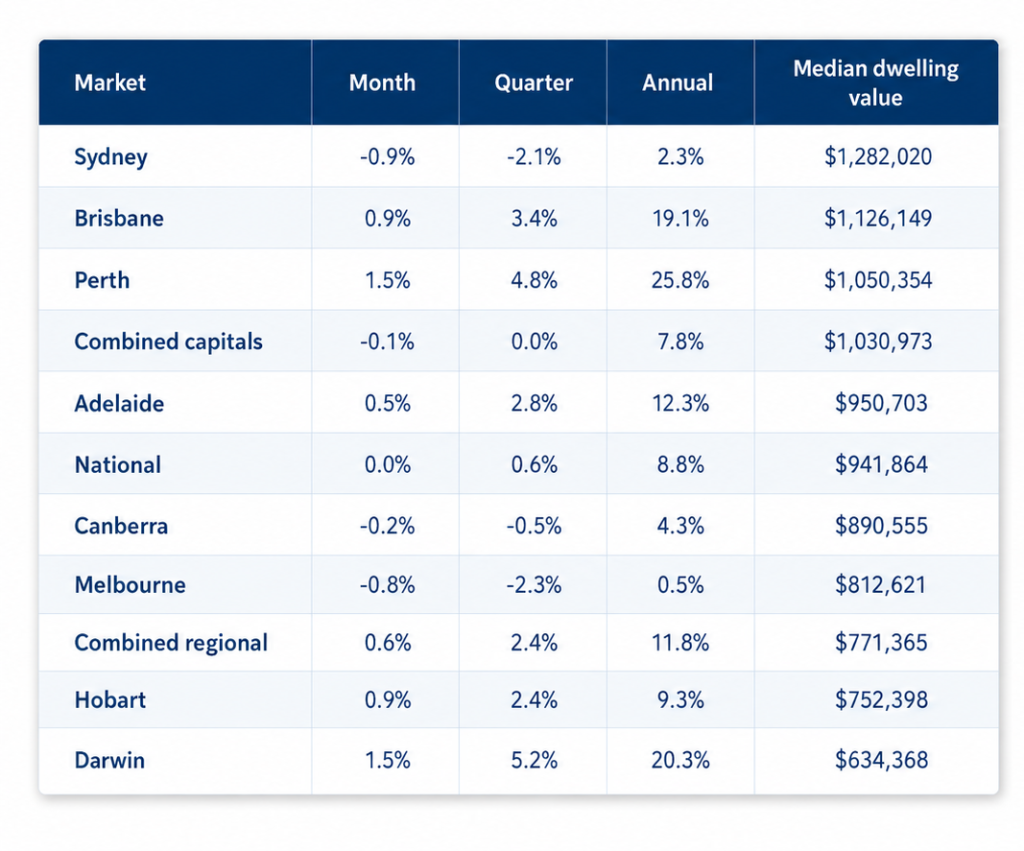

Cotality’s June HVI provides the clearest evidence yet of divergence across Australia’s capital city markets. While national values were flat in May, the result was far from uniform. Sydney recorded the sharpest monthly fall, down 0.9%, followed by Melbourne, down 0.8%. By contrast, Perth and Darwin both rose 1.5%, Brisbane and Hobart increased 0.9%, Adelaide rose 0.5%, and Canberra eased slightly, down 0.2%.

The quarterly data reinforces the extent of this split. Sydney is now down 2.1% and Melbourne 2.3% over the rolling quarter, while Darwin, Perth, Brisbane, Adelaide and Hobart have all continued to record positive growth.

The market has clearly moved beyond broad-based growth and into a period of genuine segmentation. Local economic conditions, affordability, supply levels and buyer confidence are now driving very different outcomes across the country.

Cotality’s five-year data also highlights the scale of divergence across the capital cities. Perth values are now 91.4% higher than five years ago, Brisbane is up 80.6% and Adelaide 75.3%, while Melbourne is only 3.3% higher over the same period.

That is an extraordinary spread, and it helps explain why affordability pressures are now playing out so differently across the country. In some markets, rapid growth has created real capacity constraints for buyers, while in Melbourne, relative value is becoming an increasingly important part of the opportunity.

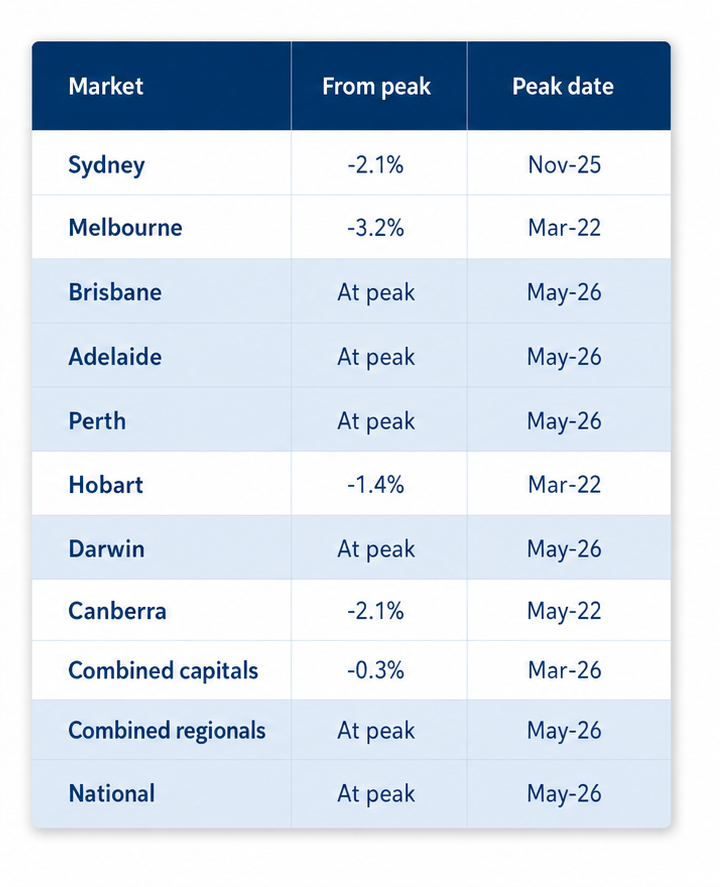

Peak versus current value

The peak-value data is also instructive. Brisbane, Adelaide, Perth, Darwin and most regional markets are now at record highs, including regional NSW, Victoria, Queensland, South Australia, Western Australia and Tasmania.

By contrast, several major markets remain below previous peaks. Sydney is now 2.1% below its November 2025 peak, Melbourne is 3.2% below its March 2022 peak, Hobart is 1.4% below its March 2022 peak and Canberra is 2.1% below its May 2022 peak. The combined capitals index is also sitting 0.3% below its March 2026 peak.

This reinforces the multi-speed nature of the current market. Some markets are still extending the cycle, while others are offering relative value after a period of adjustment.

For buyers, that creates a meaningful opportunity, particularly for those focused on high quality, well located property with strong long term fundamentals. For sellers, it reinforces the importance of anchoring price expectations in current local conditions, rather than relying on the national headline.

Melbourne and the premium market

Melbourne remains one of Australia’s most nuanced housing markets. It is not distressed, but nor is it carrying the same momentum currently evident in Brisbane, Perth or Adelaide. Cotality recorded a 0.8% fall in Melbourne dwelling values in May, a 2.3% fall over the rolling quarter and modest annual growth of 0.5%, with the median dwelling value now sitting at $812,621.

For buyers of quality homes, this presents a meaningful window of opportunity. Melbourne’s long-term fundamentals remain compelling. Population growth, ongoing migration and the continued appeal of established inner and eastern suburbs all support the outlook for well located, A grade property over time. While short term sentiment is cautious, the structural demand for scarce, high quality family homes in Melbourne’s best suburbs has not disappeared.

The premium inner and eastern markets continue to behave differently to the broader market. In Stonnington, Boroondara and surrounding blue chip suburbs, quality, scarcity and location remain the key drivers. Buyers are active where a home is well positioned, well presented and realistically priced. However, the days of broad based urgency have eased. Buyers are more selective, better informed and increasingly prepared to let a campaign pass if pricing is too ambitious.

This is a market that rewards discipline. For sellers, success depends on clear price guidance, strong presentation and a campaign strategy that understands where genuine demand sits. For buyers, the current environment offers the chance to secure high-quality Melbourne property without the same level of competitive pressure seen in stronger growth cycles.

This is where Abercromby’s is particularly well placed. A more selective market rewards experience, discretion, campaign discipline and deep buyer relationships. It is less forgiving of generic process, poor price guidance or weak negotiation.

Regional resilience and Hobart

Regional markets have continued to outperform the combined capital cities, with values rising 0.6% in May, 2.4% over the quarter and 11.8% annually. Regional Western Australia remains the standout, while Queensland and Tasmania also continue to record strong annual growth.

Hobart is also showing encouraging momentum. Dwelling values rose 0.9% in May and 2.4% over the quarter, with annual growth of 9.3%. The median dwelling value now sits at $752,398. While Hobart remains 1.4% below its March 2022 peak, the recent data points to a more constructive market after a period of underperformance and adjustment.

The longer term outlook is also becoming more compelling. Relative affordability, lifestyle appeal and Tasmania’s strong sense of identity continue to support buyer interest, particularly from those seeking quality of life without the pricing pressure of larger east coast capitals. Hobart remains a city of genuine scarcity, with limited premium housing stock, tightly held established suburbs and a natural constraint on supply.

The arrival of the Tasmania Devils and the development of the new Macquarie Point stadium add another important layer to Hobart’s growth story. Beyond sport, these projects have the potential to lift confidence, attract investment, support tourism and hospitality, and further strengthen Hobart’s profile as a capital city with national relevance. Major civic infrastructure of this nature can help shift perception, and perception matters in property markets.

Abercromby’s entry into the premium Hobart market in January 2026 is already proving well timed. The response to our brand has been extremely positive, reflecting a clear appetite for trusted advice, discretion and high quality representation in Hobart’s luxury market. As momentum returns and long term fundamentals strengthen, our early entry is beginning to pay rewards and positions Abercromby’s well for future growth.

Rental market: tight, expensive and still rising

The rental market remains tight, although affordability pressures are becoming more evident. Cotality reported national rents rose 0.6% in May, with annual rent growth now 5.9%, the strongest annual increase since September 2024. Vacancy remains the central issue, with the national vacancy rate dipping to 1.5%, in line with the record lows seen in 2022 and 2023.

There is, however, a limit to what tenants can absorb. Renters are now dedicating around a third of pre-tax income to rental payments, with the cost of renting up approximately $204 per week over the past five years. This suggests rental pressure may increasingly drive behavioural change, including larger households, more shared accommodation and delayed household formation.

For investors, rising rents and softer value growth are beginning to lift yields. The combined capitals gross rental yield is now 3.45%, its highest level since June last year, while Melbourne’s gross yield of 3.87% is the highest among the major capitals and Melbourne’s strongest reading since August 2013.

Within the premium rental market, conditions remain particularly competitive. High quality family homes and well-located residences in Melbourne’s inner and eastern suburbs continue to attract strong tenant demand, particularly where properties are well presented, secure, low maintenance and close to leading schools, transport and lifestyle amenity.

This is the segment where Abercromby’s remains focused. Premium tenants are discerning, but they are prepared to pay for quality, convenience and confidence. For landlords, strong presentation, accurate pricing and experienced management remain critical to securing the right tenant and protecting long term asset performance.

Outlook

Some demand-side headwinds are becoming more visible, with value growth easing, sales activity moderating and selling conditions beginning to favour buyers in selected markets. At the same time, there are still important supports in place. New housing supply remains constrained, population growth continues to underpin demand, and employment conditions, while softer, are still providing a degree of household income resilience.

For sellers, the market still has depth, but success will depend on discipline. The strongest campaigns will be those that meet the market early, present the property beautifully and create genuine competition among qualified buyers.

For buyers, conditions are becoming more constructive. In some markets there is more choice, less urgency and greater scope to negotiate, particularly where vendors remain anchored to last year’s expectations. The opportunity is not universal, but for well-advised buyers, it is real.

For Abercromby’s clients, this is a market that rewards clarity, experience and trusted advice. In a rising market, momentum can do much of the work. In a more selective market, the quality of the agent, the quality of the strategy and the quality of the negotiation make all the difference.